I’m talking today about a saving I’ve made in my health life, with a voucher code it works out at an even better deal 💷

One of my friends at Bannatynes is an instructor and personal trainer (PT) and we had been talking on and off for ages about nutrition. It’s taken me a while, but I recently bought a customised meal plan from him which is working really well.

Before Tom created this plan for me, I gave him a few ideas of things I like so that he could try and integrate them. Amongst those is Grenade Carb Killa protein bar.

Carb Killas come in some great flavours including Jaffa Quake, Dark Chocolate and Raspberry but my absolute fav is Chocolate Chip Salted Caramel.

Proper decent flavour!

As much as I love these bars, they are like £2.50 each and my food bill would be huge if I were to buy these from Sainsburys or similar.

They are available on subscription from Amazon and work out around £1.50 each. However, I have found similar bars at MyProtein where there are called Carb Crushers.

A box of 12 bars using the current coupon code at the time of writing brings the cost down by £5.72 to £13.34. This then works out at a pretty decent £1.12/bar.

Another good thing about buying from MyProtein is that you can collect points to use as money off in the future, and they pretty much always have offers on such as a discount or spend X and get a free t-shirt.

If you don’t have an account with MyProtein then use my link (aff. link*) and create yourself an account. If you spend over £35 then you’ll be given free delivery for three months plus I’ll get a little thank you credited to my account 😁

Also, if you go to TopCashBack and create an account (aff. link*), not only will you get a £5 bonus but you can then search for MyProtein, you can get up to 12% cashback.

I thought it might be interesting to share the structure of my main portfolio – this is where I have calculated the percentage break-downs for different markets based on my level of comfort.

There are several rules of thumb for determining the split between equities and bonds such as subtracting your age from 100 to give you the bonds (your age) and equities (the remainder) split.

As I didn’t get started with FIRE until “late on” i.e. my forties, I have gone for a more aggressive split of 20% bonds/80% equities.

At the broadest level, my equities are made up of 85% global and 15% emerging markets.

This is then diversified like:

25% Domestic

50% Developed World

15% Emerging Markets

10% Global Commercial Real Estate

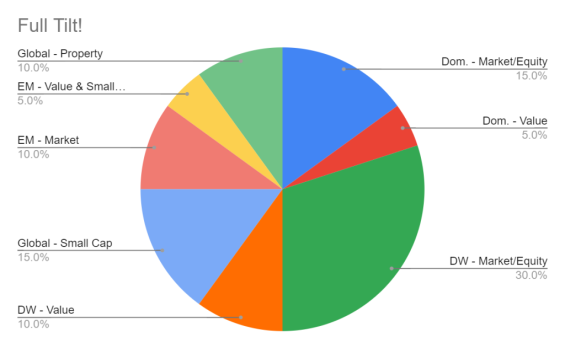

Finally, we can take a look at the tilted version of my portfolio. The percentages might look a little odd with the decimal place but I haven’t figured out how to sort that yet, the table values look fine but must have some formatting applied. Anyhow…

And with bonds included in the mix.

The actual current holdings in my portfolio are shown below, you’ll notice that there are a few areas that I am yet to invest in. I need to do more research in these areas and identify suitable trackers/ETFs.

Domestic

Market/Equity

Vanguard FTSE 100 ETF (Dist)

VUKE

SPDR S&P UK Dividend

UKDV

Value

Vanguard FTSE 250

VMID

Small Cap

??

Developed World

Market/Equity

Vanguard FTSE All-World ETF (Dist)

VWRL

Value

??

Small Cap

??

Global

Small Cap

Blackrock Global Smaller Companies

BRSC

Emerging Markets

Market

Vanguard Emerging Markets ETF

VFEM

iShares Core MSCI Emerging Markets ETF (Acc)

EMIM

Value & Small Cap

??

Global Commercial Real Estate

Property

iShares Developed Markets Property Yield (Dist)

IWDP

Bonds

Short-dated, high quality bonds

Vanguard UK Gilt ETF (Dist)

VGOV

Short-dated, high quality, inflation-linked bonds

iShares Indexed UK Gilts

INXG

It would be good to hear how your portfolio compares to mine by way of split and how you decided on the allocation of equities and bonds.

The following post is contributed by Martin of Studenomics, where he tries to make personal finance fun since you have enough to stress about. You can click here to check out the wide range of content on everything from student loans to getting paid to drink coffee.

Are you looking to start your first side hustle? Are you excited about the idea of making money on your own?

I think you’ll agree with me that there’s a lot of confusing information out there about making money. You start reading about one income source and then end up with an information overload. You don’t know if it’s all a scam or if you’re missing out on an opportunity of a lifetime.

Keep on reading if you want to know what to look for in a side hustle so that you don’t spend the next six months stuck at day one…

Quiet month for me in general so I’ll crack on with things…

Additional Income Streams

Matched Betting £137 (Oct £275)

Surveys/studies £10.21 (Oct £16.56)

Things were a bit slower this month with my matched betting although I still made a >£100 profit which I’m fine with. I wasn’t feeling it for a good while so just dipped in and out as I fancied it.

How did I do in November?

Assets

Emergency Fund £1,150.80 (£1,107.69)

ISA, Freetrade £3,546.79 (£2,187.76)

ISA, Hargreaves Lansdown £2,682.73 (not recorded)

Pensions £97,194.47 (£94,943.49)

SAYE £390.00 (£360.00)

House £350,883 (not recorded) *HPI current valuation

Liabilities

Credit Card -£1,728.26 (-£2,299.60)

Student Loan -£3,806.77 (-£3,960.77)

Mortgage -£189,487.04 (-£190,668.62)

Total Assets (excluding house) – Total Liabilities = Net Worth £104,964.79 – £195,022.07 = -£90,057.28

Yes, I have a big mortgage and the repayments are pretty hefty but the decisions around that were made pre-FIRE journey.

We could downsize as we have a spare bedroom and an office/5th bedroom but when we looked into this a few years ago there just wasn’t much to gain if we want to stay in the current area. We’re not looking to relocate just yet as my daughter is in her final year at high school and then hopefully starting college. Renting out the spare room could be an option we considering though…

It’s not something I’d rule out in the future as I like the idea of geo-arbitrage although that comes with other considerations such as having the best dog in the world that we would have to take with us as I’d not even think about giving her up.

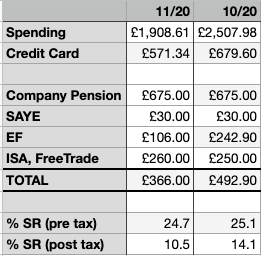

Month-on-month

As you can see, although my spending and credit card payments are down this month, my savings rates are down too. Part of the reason for this is a bit of lethargy, I just struggled with motivation to bring in extra money which would have been used to reduce debt and increase savings.

Thankfully, my credit card payments should be done with ahead of schedule – it’s now looking like the bulk of the balance should be cleared in December and then January will mop up the remaining balance.

Whether then to start on paying down my Student Loan or to add to my Emergency Fund is the question. My Student Loan is under £4,000 and attracts a rate of interest of 2.6%.

I’d be interested in hearing your thoughts on this – would you clear the loan and be rid of all debt (except mortgage) or build your EF a bit more?

Future Fund

Continued good performance from my Scottish Widows pension scheme and a boost to the Freetrade ISA saw me edge past the £100,000 milestone.

So happy about this as it is the first big milestone that I have hit on my way to FIRE 🙂

Also, just while compiling my list of assets and liabilities/debts (above), I realised that I have not included my HL ISA in my Future Fund so that’ll be added from December onward.

I have set the next milestone at £150k which I plan to make in the next couple of years. Increased pension contributions, both from higher saving rate & higher salary, plus side hustles and general market performance although the latter cannot be relied upon.

Yay! I’ve awarded myself a badge 😀

Started recording my dividend payments in my Freetrade ISA (lazy portfolio) which can be seen in the graph below. I’ll provide a breakdown of my lazy portfolio in the future showing what funds I have.

Dividend Payments

Not likely to be retiring any time soon on the above level of payments but I expect these numbers to grow nicely over time. I’ve set an informal target of the monthly dividends being enough to cover my mobile phone payment which is not much, like £5, so should hopefully be achievable in the next 12 months. I’ll then add the next notional target – over time the goal is to have the dividends covering a significant proportion of my regular expenses.

Credits

I have taken inspiration and assistance from a couple of other FIRE bloggers in the creation of my monthly updates so I’d like to take the opportunity now to say thank you.

Weenie over at QuietlySaving – thanks for providing quality posts, yours was the first FIRE blog I started reading and it was from your updates that I “borrowed” the Future Fund concept. Also a big thank you for your help with my dividend graphing (see above) – I was banging my head against the wall with Apple Numbers trying to get it right, I then went from Excel (thanks!) to Google Sheets and I’m pretty happy with the result.

You can read what Weenie’s November looked like here.

Sassenach Saving‘s monthly updates provided me with the thought of breaking down my assets and debts for a month-on-month comparison. Check out their November update here.