The following post is contributed by Martin of Studenomics, where he tries to make personal finance fun since you have enough to stress about. You can click here to check out the wide range of content on everything from student loans to getting paid to drink coffee.

Are you looking to start your first side hustle? Are you excited about the idea of making money on your own?

I think you’ll agree with me that there’s a lot of confusing information out there about making money. You start reading about one income source and then end up with an information overload. You don’t know if it’s all a scam or if you’re missing out on an opportunity of a lifetime.

Keep on reading if you want to know what to look for in a side hustle so that you don’t spend the next six months stuck at day one…

Quiet month for me in general so I’ll crack on with things…

Additional Income Streams

Matched Betting £137 (Oct £275)

Surveys/studies £10.21 (Oct £16.56)

Things were a bit slower this month with my matched betting although I still made a >£100 profit which I’m fine with. I wasn’t feeling it for a good while so just dipped in and out as I fancied it.

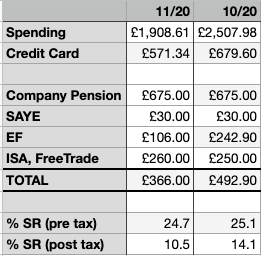

How did I do in November?

Assets

Emergency Fund £1,150.80 (£1,107.69)

ISA, Freetrade £3,546.79 (£2,187.76)

ISA, Hargreaves Lansdown £2,682.73 (not recorded)

Pensions £97,194.47 (£94,943.49)

SAYE £390.00 (£360.00)

House £350,883 (not recorded) *HPI current valuation

Liabilities

Credit Card -£1,728.26 (-£2,299.60)

Student Loan -£3,806.77 (-£3,960.77)

Mortgage -£189,487.04 (-£190,668.62)

Total Assets (excluding house) – Total Liabilities = Net Worth £104,964.79 – £195,022.07 = -£90,057.28

Yes, I have a big mortgage and the repayments are pretty hefty but the decisions around that were made pre-FIRE journey.

We could downsize as we have a spare bedroom and an office/5th bedroom but when we looked into this a few years ago there just wasn’t much to gain if we want to stay in the current area. We’re not looking to relocate just yet as my daughter is in her final year at high school and then hopefully starting college. Renting out the spare room could be an option we considering though…

It’s not something I’d rule out in the future as I like the idea of geo-arbitrage although that comes with other considerations such as having the best dog in the world that we would have to take with us as I’d not even think about giving her up.

Month-on-month

As you can see, although my spending and credit card payments are down this month, my savings rates are down too. Part of the reason for this is a bit of lethargy, I just struggled with motivation to bring in extra money which would have been used to reduce debt and increase savings.

Thankfully, my credit card payments should be done with ahead of schedule – it’s now looking like the bulk of the balance should be cleared in December and then January will mop up the remaining balance.

Whether then to start on paying down my Student Loan or to add to my Emergency Fund is the question. My Student Loan is under £4,000 and attracts a rate of interest of 2.6%.

I’d be interested in hearing your thoughts on this – would you clear the loan and be rid of all debt (except mortgage) or build your EF a bit more?

Future Fund

Continued good performance from my Scottish Widows pension scheme and a boost to the Freetrade ISA saw me edge past the £100,000 milestone.

So happy about this as it is the first big milestone that I have hit on my way to FIRE 🙂

Also, just while compiling my list of assets and liabilities/debts (above), I realised that I have not included my HL ISA in my Future Fund so that’ll be added from December onward.

I have set the next milestone at £150k which I plan to make in the next couple of years. Increased pension contributions, both from higher saving rate & higher salary, plus side hustles and general market performance although the latter cannot be relied upon.

Yay! I’ve awarded myself a badge 😀

Started recording my dividend payments in my Freetrade ISA (lazy portfolio) which can be seen in the graph below. I’ll provide a breakdown of my lazy portfolio in the future showing what funds I have.

Dividend Payments

Not likely to be retiring any time soon on the above level of payments but I expect these numbers to grow nicely over time. I’ve set an informal target of the monthly dividends being enough to cover my mobile phone payment which is not much, like £5, so should hopefully be achievable in the next 12 months. I’ll then add the next notional target – over time the goal is to have the dividends covering a significant proportion of my regular expenses.

Credits

I have taken inspiration and assistance from a couple of other FIRE bloggers in the creation of my monthly updates so I’d like to take the opportunity now to say thank you.

Weenie over at QuietlySaving – thanks for providing quality posts, yours was the first FIRE blog I started reading and it was from your updates that I “borrowed” the Future Fund concept. Also a big thank you for your help with my dividend graphing (see above) – I was banging my head against the wall with Apple Numbers trying to get it right, I then went from Excel (thanks!) to Google Sheets and I’m pretty happy with the result.

You can read what Weenie’s November looked like here.

Sassenach Saving‘s monthly updates provided me with the thought of breaking down my assets and debts for a month-on-month comparison. Check out their November update here.

October was a pretty decent month for me; personally, professionally, and financially.

In work, I got my promotion (finally) confirmed and a nice, chunky pay rise which was due to the promotion but also bringing me more toward market value.

Like most people, I already had plans for what I’d do with my extra pay but being on my journey to FI I didn’t pre-order a whacking great big TV or sign-up to lease a new car, instead I put a plan in place to use the money to pay down my debt faster.

I should now be able to clear my credit card debt within five months which will be awesome. Will be the first time in as long as I can remember that I’d not owe money on a card. Also, this month I’ve been making additional payments to my card which is shown in the table below.

Once the card is paid off, I’ll shift my attention to my student loan, thankfully it is small (around £4k) but it will still take a little while to pay off. Probably around this time next year it should be dealt with which will leave me with the extra money plus £140/month more which is currently deducted automatically from my salary.

Toward the start of the month, I decided to get rid of my loan I took out when I purchased my new phone. The balance was £434 and has resulted in a monthly saving of £29, or just under £350 a year 🙂

Matched Betting

I thought October was going to be a struggle in terms of making much profit but it turned out to be pretty decent by my terms.

The profit in the first two weeks alone passed that for the whole of September, a fair proportion of that was from taking the boosted odds from the likes of Ladbrokes and William Hill each day. A lot of small gains added up nicely.

For the first time, I withdrew some profits from my matched betting ecosystem, this was used to reduce my credit card balance. I’ll need to take some more funds from my exchange accounts and redistribute it across some of the bookies as a lot of the funds have flowed the other way.

Also tried a few accumulators, mainly as a learning exercise, but I think out of about five or so only one returned a small profit. As fellow matched better, weenie warned me, it’s hard at the moment to make anything from an acca as the football results are all over the place.

It’s great that football has returned and individual fixtures can still throw profits, especially when you get free/risk-free bets, but trying to string together results in an acca is a totally different proposition.

Holiday – yay!

Having had pretty much no real break from work this year, I attended an annual golf weekend on the North Norfolk coast. This I think is the fourth year running that we have stayed and played at Heacham Manor although I had to cancel last minute in 2019.

It was nice to get away and spend some time with friends some of whom I have not seen for a couple of years.

We always start off with a coffee and bacon roll in the clubhouse before getting in a round and unlike 2018, the weather wasn’t too bad. Despite being windy and wet for the first three holes, it eased up and toward the end, it was actually warm enough to take off my water proof jacket!

The evenings are always fun too. I shared a cottage apartment with one of my best mates and spent a good while chatting and drinking G&Ts before heading to the restaurant for the three course meal. We had to split into two groups due to social restrictions but that was fine.

Tempura prawns

Steak

Millionaire cheesecake

I didn’t play any golf in the morning before coming home although some of the guys did stop around for that.

We also had a long-awaited family holiday to a cottage in a village outside Nottingham. Having originally booked for the four of us plus Skyla, my son had his shifts come through for his new job which meant he wasn’t able to come 🙁

I had looked to see if we could postpone this break as there was talk of Nottingham going into tier 3 but nothing confirmed so the booking company wouldn’t have been able to help. I’m glad we went though, the cottage was lovely – small but really cosy, and it was nice to have a change of scenery.

Skyle endorses Ikkle Cottage

Wooded Path

The Black Bull

It rained on and off each day but we still got out for walks with Skyla and had a few pub lunches/dinners. Was good to spend some time with Freya away from home, she managed to tear herself away from her phone a few times and join in the conversations.

We ended up leaving a couple of days earlier than planned as the whole county was due to be locked down and placed into tier three, that, plus the rain and a slightly moany teenager kind of told us it was time to come home!

Additional Income Streams

Matched Betting £275 profit (Sept £158)

Surveys/studies £16.56 (Sept £17.99)

Up to the end of October, I have made just over £53 from Prolific surveys, not game-changing but it all counts and it’s the time when I’m not particularly active and just unwinding.

Still not been able to pass any pre-qualifying checks for UserTesting, might continue trying with this for a while longer and see how it goes.

Well pleased with matched betting profit for last month. Between the surveys and matched betting profit in October, I was able to pay off an extra £300.

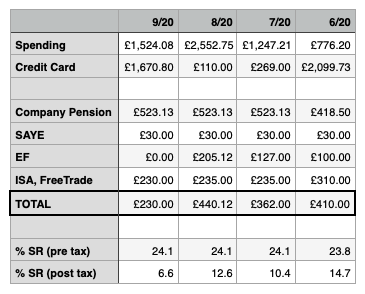

How did I do in October?

Notably, this month were expenses coming in at just under £900 on the holiday in Nottinghamshire, this covered the balance of the rental cottage, groceries, eating out and some clothes shopping for my daughter 🙂

It’s nice to see my pension contributions increase this month, my percentage rate has remained the same just that I’m now getting paid a bit more 🙂

Slightly increased amount added to my ISA this month, I think this will remain pretty static until I get some debts cleared.

It’s frustrating having to divert money from savings/investments to pay off debt but I don’t want to beat myself up about it as my life is different since finding FIRE.

My combined saving rate of 39.2% is pleasing, it’s encouraging me to keep working at the three pillars – cutting expenses, earning more, and saving more.

Future Fund

Another good month for my pension as that has gone up £3,500 since September. Not sure what it will look like at the end of November though as the US Presidential election would have taken place which may impact the market. Still, that’s not in my sphere of influence so I’m not going to worry about it.

I’m starting to think as to whether an end-of-year review is something worth doing, summing up any highlights as well as my progress to better financial health.

Is this something that you do/have done in the past? Do you find it useful? Would love to hear your thoughts in the comments section below.

It was a tough month at work, sometimes despite having loads to do I can find it hard to keep going. The work is typically varied and normally it keeps me interested but perhaps it was the change in weather or completing a challenging task that left me feeling a bit down, I’m not sure. This then rolled into me developing a sore throat and then a list of other symptoms which scarily sounded a lot like COVID-19.

I decided to take sick leave and self-isolate but as things didn’t improve I booked myself a test, I make it sound easier than it actually was – it turned out to be pretty hard to book any kind of test! Despite having a drive-in testing centre about a mile from my house I had to wait three days before I was finally lucky enough to get offered a home testing kit.

After getting the test kit ordered, the rest of the process was pretty decent. The kit arrived the next day, I then got it returned the same afternoon and within two days I got the result back which was thankfully negative. The odd thing though with the fam self-isolating is that my daughter was actually put out about having to stay off school! 😀

One downside to being ill was that it interrupted my gym routine and I don’t mean that in a vain way, it is one of a few things that keeps me well balanced and in a reasonable state of wellbeing. Thankfully after a week and a bit off while the symptoms cleared, I was able to go back and restart the classes.

I managed to spend a fair bit of time this month reading and listening to audiobooks, not all personal finance-related, I enjoyed listening to The Amityville Horror although I had to replay a lot as I kept dozing off during it! It’s a good book though and I’d recommend borrowing a copy from the library.

Also, I took some produce from the garden…

Not a huge amount, the potato plants are still growing as are the pears so will provide more in the months to come. The pears are actually pretty large, the photo doesn’t really do them justice, in fact they are large enough that they have caused the tree to lean over so I should really start picking some more!

At the same time as the potatoes, I also planted some onions but they grow much slower so won’t really be ready until maybe Decemeber. I have taken a couple up though and used the to add to a salad as I planted a mixture of red and white. The carrots didn’t survive due to Skyla digging them up before they could get established.

The apple tree was reasonably fruitfull this year and have contributed to a good few apple crumbles. We also have a dwarf pear tree in the front garden which typically is pretty decent but nothing this year.

All good stuff though, food on the table and some fresh air & fun prepping, planting and picking 🙂

Additional Income Streams

Matched Betting £158 profit (Aug £168)

Surveys/studies £17.99 (Aug £19.27)

I didn’t take out any profit from my matched betting but the survey profit I used to reduce my credit card balance.

While off ill, I was looking at ways to bring in extra income and I came across JustPark. This company (I’m sure there are others too) allow you to rent out any car parking space (or garage) that you don’t need and also help you find parking if you are visiting somewhere. If you sign-up via my referral link* and rent out your space then we both get £10 to spend on parking, or a £10 Amazon card.

No takers yet but it is not surprising with the lockdowns and large numbers of people working from home. In the future I may get a bit of business if the larger Aviva offices reopen and people start coming back but we’ll see, I’m not losing anything by making it available.

Matched Betting

Completed all the easy new account offers via Odds Monkey so I’m now starting with the average difficulty ones. The fact that all the easy ones are done has had an effect on my monthly profit, that and making a few mistakes. I’m still learning so I expect to mess a few bets up so I’m not too cut up about that.

I’ve been chatting with Weenie about accumulators so that is something I’ll be trying out in October, not sure what the results will look like but hopefully gain more profit than I lose.

Also opted to switch to annual renewal for my OddsMonkey membership, this was a pretty decent result as 12 months was being offered at £140 (£10 saving) compared to £15/month.

How did I do in September?

Spending was down significantly compared to last month as there were no large expenses to sort out.

I didn’t add any further contributions to my Emergency Fund as I put that, together with savings from spending, and paid down a decent wedge on my credit card balance.

It’s such a good feeling seeing the credit card balance edging nearer to zero. Once I’ve got this paid off I’ll have to decide whether to start paying off my student loan or the smallest part of my mortgage (it’s made of up four parts; two at a lowish rate and two at a higher rate).

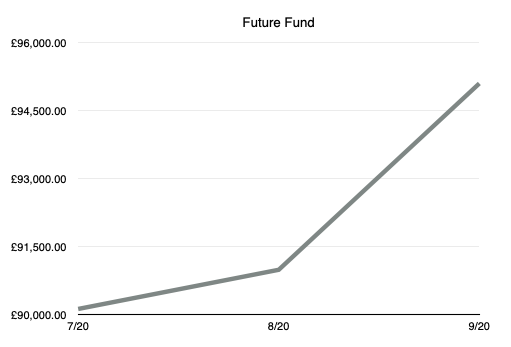

Future Fund

Yay! First graph for my Future Fund 😀

Contributions to my Future Fund via Pension, EF, and ISA didn’t change much with the exception of the EF payment as mentioned previously.

The sharp rise during September is down to the inclusion of an ISA and also an uplift of just over £2700 in my pension.

It will be cool to pass the £100k mark although that could take a little while yet but seeing this graph and my decreasing debts are giving me a ton of motivation to keep pushing ahead.

I finally got around to booking a holiday for the family, we found a nice little place near Ravenshead, Nottinghamshire. The same cottage was available on several websites but I opted for dogstrustholidays.co.uk as they get a percentage of the fee to help with the good work they do.

Really looking forward to this break as it’s the first holiday I would have had in four years. As our son is 18, getting on for 19, it might also be the last family holiday we have together before he starts his lads holidays.

Being able to take our dog, Skyla, with us too is great – she will love the change in scenery and there are plenty of places to walk and also dog-friendly cafes and pubs. This will be her longest trip in the car so we didn’t want to book anything too much further from home for that reason, I think it should take around four hours to get there with a few stops so she can stretch her legs.

I reckon it will be nice to get away, going for walks in new and exciting places will be fun for me as well as Skyla (plenty of dog-friendly pubs and cafes apparently)!

Skyla in the nearby woods

Work

The month of August, along with September, is one of the busiest times of the year for the product group I am part of. Many colleges and universities are preparing to welcome students back and with that, we see a spike in users of our mobile app. This is great but it also presents some challenges for us…

Ensuring that the platform that the app sits on is reliable and robust enough for the volume of users is one of the main duties of my role. We had a little blip around results day in the UK and we’re doing what we can to try and prevent something like this from reoccurring around admissions time. Consequently, it feels like a lot of my time has been spent around reviewing logs and looking at performance graphs as well as working with developers to resolve anything obvious.

The above, coupled with resource planning and liaising with other teams, can mean that I have little time to progress other requests like implementing new customers. This can get me down and I definitely recall entering a spell of depression as the month ended despite having booked the previously mentioned family holiday.

My thoughts have been heading in the direction of “what can I do to change things”, this did make me feel grateful that I had come across FI/RE and the realisation that there are options available. Exploring other ways to generate income is an ongoing process for me, as you’ll see in a moment.

Here are my numbers for August:

Monthly Figures August 2020

I thought I’d start including my pre-tax and post-tax saving rates, mainly so when I read/hear about other people’s savings rates I have idea of what that looks like comapared to mine.

I’m not using the numbers in a bad way, as a direct comparison, where I can beat myself with a stick over them. It’s more for interest.

Also, the pre and post-tax rates are there as I think they give a better indication rather than just trying to use one set of numbers. It feels more representative in my eyes.

Is calculating your savings rate something that you do, if so, do you work with just one figuring or do you have pre-tax (gross) savings that you make?

I didn’t get to pay too much extra off my credit card this month, mainly due to the increased spending levels. Some of the things that contributed to a high level of spending were:

£160 – Overnight stay with my wife at the Wayford Bridge Inn, somewhere we like to go back now and again, and is just a short distance outside of Norwich. We were also able to take advantage of the “Eat Out to Help Out” offer which was handy 🙂

£565 :^O – This was for renewing the road tax for my car, I had declared it off-road (SORN) and so paid out for 12 months. This one hurt but in my defence, I hadn’t discovered FI/RE or frugality when I bought this car.

£102 – Train ticket for my wife to visit a friend in Shropshire.

£31 – Not a huge amount but something I hadn’t budgeted for was a book from Gumroad.

Additional Income Streams

Matched betting £168 profit

Surveys/studies £19.27

I didn’t get round to listing anything on eBay this month and I’ve sent in all the stock I had for Amazon FBA so there’s nothing new to report on there.

This was my first month of matched betting and it’s something I’m enjoying a fair amount. The profit mentioned above has all stayed within my matched betting “ecosystem”, the money I have deposited in various bookie and betting exchange accounts has moved around as a loss in one place results in a gain in another. The gains can occur on either side of the equation, when I get a reasonable win with a bookie I withdraw some funds and deposit that at the exchanges – being able to carry a high(er) liability allows me to place more bets.

This month I also signed up to Prolific, an online survey provider. I became aware of them from Vicky aka Mortgage Free by the Sea – check out the review on her blog. Essentially, you sign up, complete a load of questions about yourself and then wait for studies to become available. Each one offers a different amount which usually corresponds to the effort required to complete them

Although a fraction under £20 doesn’t sound like much, it’s an okay return on the time I put into it. Most of the studies I have completed have been in the evening when I’ve been in the lounge relaxing so it’s hardly an inconvenience. The proceeds from Prolific will either end up in my Freetrade ISA or my Emergency Fund.

Future Fund

Seond month of monitoring my Future Fund and the value has increased by just over £862 to £90,993. I’ll probably pop in a graph next month when I’ve got another set of numbers to add in.

I am contemplating selling some of my FAANG shares currently held with Hargreaves Lansdown in order to invest the proceeds in trackers & funds with Freetrade, I’m up between £100 and £350 on each of the holdings and I currently think keeping a fair amount of money tied up in tech is not necessarily the safest option.

It is interesting having shares in big tech companies, and Uber, but I know that I’ll feel safer and more confident about my financial future knowing that the money is silently working away for me in trackers/funds rather than all the glam and after parties of Facebook, Netflix etc.

The entire workforce was put onto 80% time/salary at the start of May as a precautionary step to protect the financial wellbeing of the company. I was initially worried about the financial impact this reduction in hours would bring but we have coped fine thankfully, my wife picked up extra shifts so it lessened the blow a bit.

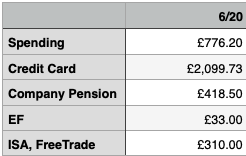

How did I perform financially? I’ve put together a few figures to try and establish some benchmarks for future months, there may be a bit more detail for some areas than others at the moment but I’m working on that.

Spending

This covers our expenses such as groceries, travel costs, pets, and any other discretionary spending for the month. Not sure how this would compare to other families of four but it is the lowest for amoutn spent in a month this year – not sure if that’s because we have been doing less or if I’ve messed up the tracking somewhere!

Travel costs are really low at the moment as my wife is cycling to work, I’m still working from home, and we have declared our car off road with the DVLA.

I anticipate a much improved accuracy for spending in July as I have taken up the use of an app called “Emma” which utilises the open banking here in the UK to amalgamate transactions and balances across mutliple accounts. More on this app in another post, but it you’d like to take a look and sign-up in the mean time, please use my link* as I earn in-app points 🙂

Credit Card

I was a little hesitant in adding this category as I feel a degree of shame about getting into credit card debt. In fact, I have carried around this type of debt since my twenties, occasionally paying off the balance in full only to build it back up again. But, as Vicki Robin says, “No shame, no blame”!

Decided to use some extra money we had to pay down the debt a bit more aggressively this month than we usually would. Feels good to see that number come down and also get the balance below 25% of my credit limit.

Having been listening to the ChooseFI podcast for a little while now, the idea of using travel reward credit cards has grown on me but I still harbour a “fear” of the cards and the trouble they can cause without sufficient will power.

Company Pension

I use salary sacrifice to make the most of my income, this reduces the amount of income tax I have to pay as my salary is effectively reduced. My company offer a 3% contribution match which I take advantage of plus I add a decent percentage on top of that.

The scheme is run by Scottish Widows and typically does okay but the 2019/2020 year ended in a negative performance percentage. This resulted in my pension pot losing a few hundred pounds despite the contributions.

Emergency Fund

Contributions to my EF were low this month, mainly because I forgot to add the money 🙁

Note to self: automate this to avoid the same happening again!

Pretty much all the podcasts and books talk about setting up an EF to cover three to six months of expenses, this feels pretty daunting when starting out. My first target is to cover one month’s worth, then I’ll aim for two months. I feel much more inclined to keep going when the goals are achievable, they don’t have to be easier but achievable none the less.

ISA, Freetrade

I opened my Freetrade ISA in May and added a further £310 to it during June. The cash balance was invested in funds according to my portfolio strategy which I’ll talk about in another post. I don’t have a magic link for Freetrade but if you are interested in opening an account (in the UK) then message me and I’ll send one through, we’ll both then earn a free share worth between £3 and £200 – nice!

That pretty much rounds out my thoughts on my June finances, a bit late in getting these written down and published but heh-ho 😀 Next month, I intend to get round to this a bit earlier and making small incrementally improvements to my systems should enable this.

Quick question for you, do you use reward credit cards? If so, what have they enabled you to do, what places have you visited courtesy of using these cards rather than using a debit card?

Thanks for making it this far! Let me know what your thoughts are on financial updates and the kinds of things you measure.