This article contains affiliate/sign-up links.

July was the first month back at full-time which was great news for my bank balance but I had kind of gotten used to working four days and having the long weekends! My team were amongst the first to go back to full-time with the developers and QAs returning the start of August.

No more lounging around in my back garden on Fridays (not really my backgarden!).

Work itself has been pretty busy since returning to a five day week, but that’s a good thing as we still have customers in the pipeline.

Several people have opted to remain at 80% as they have found it is a better fit for their circumstances, I must admit that I was tempted but it doesn’t feel like the right time just now. In hindsight, the one day off each week could have been seen as a step toward semi-retirement but I am still in my wealth-building stage and I could do with the extra pay to help meet my goals.

One of the perks my company offer is the ability to buy or sell annual leave. There are typically quite a few people that take advantage of this each year and purchase the maximum additional leave of five days.

With the COVID-19 situation though, and not being able to travel, I still have the majority of my leave left so I decided to sell some back. A couple of weeks ago I received confirmation that this had been agreed and I’ll now be credited with an additional £100/month gross to my salary each month for the rest of the year.

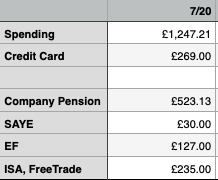

My monthly figures are shown below, generally okay in the good areas but spending was up significantly on June. The increase in my company pension is mentioned just below…

Company Pension

Before the reduced hours, I had been contributing 12% toward my company pension via salary sacrifice. I increased my rate of contribution to 15% when my salary was cut as I didn’t want to impede my pension growth. My plan is to leave my contribution rate the same going forward meaning I’ll be tucking away a bit extra month-on-month.

Additional Income Streams

In addition to my salary, I am trying to create and nurture additional income streams.

- FBA (Fulfilled By Amazon) Sales £51.39 profit

- eBay Sales £14.14 profit (June £101.65)

- Matched Betting £20.00 free bets £0 real money

eBay sales are pretty much a no-brainer, anyone can do this, and the items sold during July were all sourced from my home. I’ve currently got a stack of things to photograph and list so it’s something of a backburner task. One of the advantages of selling on eBay is their postage service – they have agreements with a few courier firms offering discounted rates which tend to be cheaper than Royal Mail. I can opt to print the postage label in store (handy as I don’t have a printer at home) and then walk to the local shop which is about 20 minutes away to drop off the item(s).

FBA takes a little more effort and this months sales were generated from a couple of sets of Joe Wicks saucepans which I had purchased from Dunelm Mill a while ago in a sale. They had been sitting around at home for ages so I finally decided to get them sent in and listed. Glad I did as they both sold within a week on being received at the distribution centre.

Matched Betting – I only just signed up for this at the very end of the month and I am still working through the tutorials from OddsMonkey* (this is weenie’s affiliate link as I’m not yet a Premium member). Thus I have only unlocked some free bets and yet to realise real money that I can withdraw and invest.

Future Fund

This is something I picked up from weenie over at quietlysaving, after finding out what it is and what kind of things it includes I have decided to start tracking my own future fund (thanks weenie!).

This month, I’ll just report the figure – seems little point in me creating a graph for just one data point! 😀 – which is £90,129. I’m pretty sure this number will increase as I have to analyse my Hargreaves Lansdown ISA as I currently have holdings there which are ring-fenced for my kids.

Included in this figure are my pensions (excluding my defined benefits pension), ISAs, and cash savings. I won’t be including my CrowdCube investments as the investments made here cannot currently be liquidated. Also excluded is the equity in my home.

What kind of side hustles or income streams do you have? I’d be very interested to hear what you are up to in order to speed up your journey to FI.

Also, if you haven’t already, find me on Twitter @ithefrugalist and give me a follow – I’ll be sure to say “hi” and follow you back 🙂

* affilitate or sign-up link